Mankato Chapter 7 Bankruptcy Attorney

Chapter 7 bankruptcy is the type of bankruptcy most people think of when they hear the

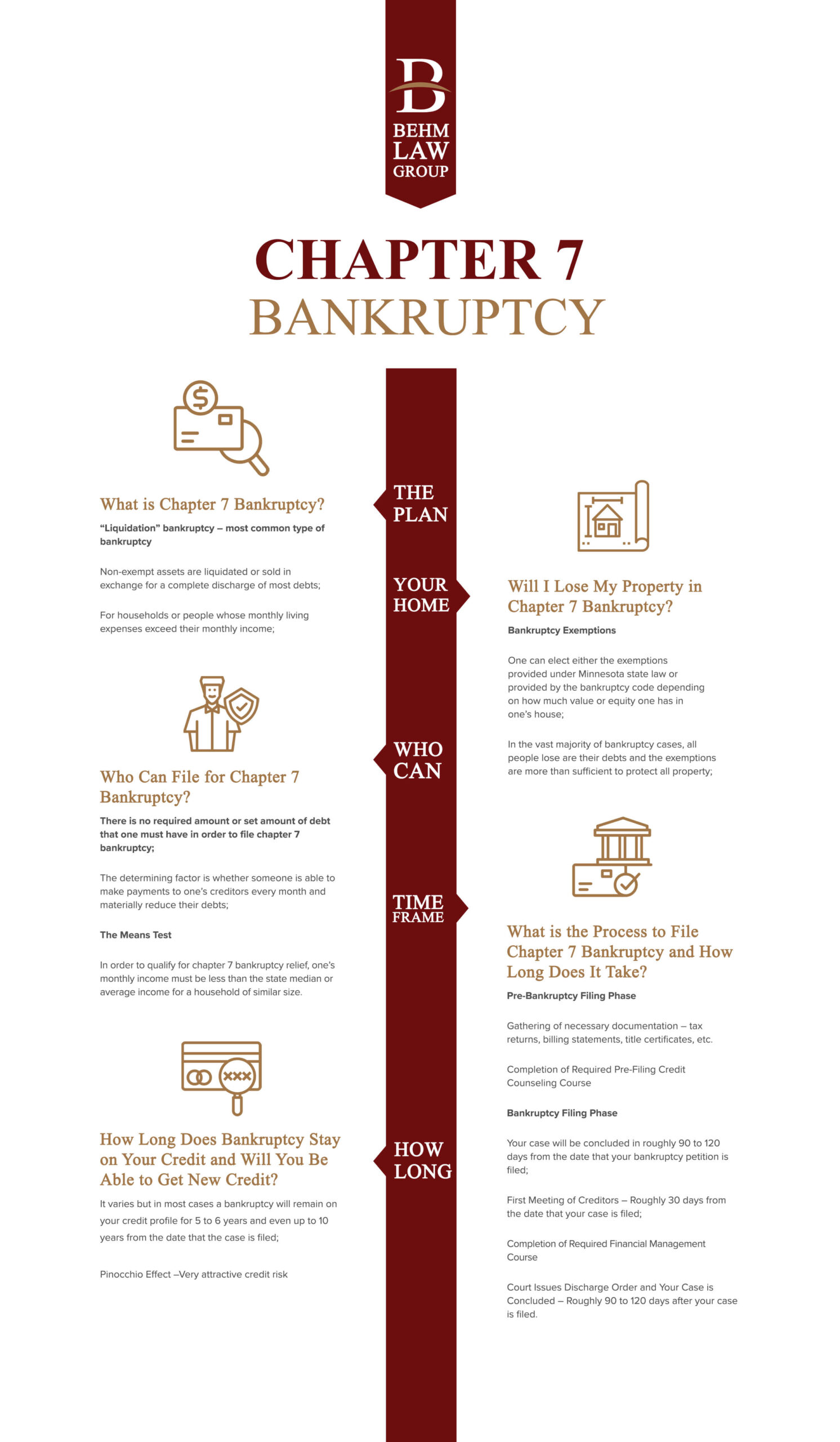

word “bankruptcy.” It is also referred to as “liquidation bankruptcy” or “straight bankruptcy.” It is the most common form of bankruptcy in the United States. In this type of case, the bankruptcy trustee collects all of your non-exempt assets (described below), sells them, and then distributes the cash to your creditors as provided by law. The result of a successful bankruptcy proceeding is the receipt of a bankruptcy discharge order. A discharge order is an order issued by the bankruptcy court which nullifies one’s pre-bankruptcy contractual obligations to pay creditors. In other words, one’s debts are discharged and one is relieved, by operation of the bankruptcy code, of having to repay them. Typically, one does not lose property because there are sufficient bankruptcy exemption laws allowing one to protect one’s property from creditors. One can usually retain one’s house mortgage and car loan as long as one is current with the payments on those obligations.

Generally speaking, a person with monthly necessary living expenses that exceed one’s net monthly income files for chapter 7 bankruptcy. In other words, if one’s living expenses such as rent/house payment, food, gasoline for vehicles, insurance for vehicles, heat and electricity and other necessary living expenses (not credit card payments or monthly medical payments or past due utility bills or overdraft protection charges attached to one’s checking or savings account) exceeds one’s net monthly income (gross income less taxes and medical insurance and other deductions) one should seriously consider filing for chapter 7 bankruptcy relief.

click to learn more about</>

CHAPTER 7 BANKRUPTCY

What Does Chapter 7 Bankruptcy Look Like?

The chapter 7 bankruptcy process usually takes between 90 and 120 days between the date a bankruptcy case is filed and the date that the bankruptcy court issues a discharge order. There will be a bankruptcy court filing fee of $306.00 that you will have to pay our office. The amount of the attorney’s fees depends largely on how complicated your case is, but our fees are very competitive. Under current law, however, all attorney’s and court filing fees must be paid in full before a chapter 7 case can be filed. The process is started by contacting our office for a free one hour consultation. Our office will give you a bankruptcy questionnaire to complete wherein you list all of your personal information such as full name, address, social security number, income and expense information, list of assets, and list of creditors. We will then prepare your bankruptcy petition and related schedules from that bankruptcy questionnaire. In addition to completing the bankruptcy questionnaire, you will be asked to provide certain documentation such as your tax returns, pay stubs, bank account statements, title certificates for your vehicles, and other relevant documentation that will allow for the complete and accurate preparation of your bankruptcy schedules.

Once we have completed preparing your bankruptcy petition and related schedules, we will need you to personally review it with one of our attorneys to verify that the information is true and accurate. After you review your bankruptcy petition and related schedules, our office will file them electronically with the bankruptcy court.

Once a bankruptcy is filed, a legal entity (much like a corporation) called the “bankruptcy estate” is created by operation of the bankruptcy code. The bankruptcy estate is, in fact, a legal being that can file tax returns, can sue people and can be sued by people. It gets managed and administered by a bankruptcy trustee (not a Judge), a lawyer appointed by the United States Department of Justice to review bankruptcy cases.

Significantly, when a case is filed, all of your property actually becomes property of the bankruptcy estate by operation of the bankruptcy code. In other words, your property does not belong to you anymore. Rather, it belongs to the bankruptcy estate. However, Congress did not want people to emerge out of bankruptcy completely destitute (wearing a barrel and suspenders, for instance) and without property to reorganize and rehabilitate. Therefore, Congress provided certain bankruptcy exemption laws that allow you to exempt property back out of the bankruptcy estate and retain it. Usually, the bankruptcy exemption laws are sufficient to allow for the retention of all of the property that was dumped into the bankruptcy estate when the case was filed.

An Automatic Stay Can Provide Relief

Once a case is filed, the automatic stay goes into effect. The “automatic stay” is a legal provision of the bankruptcy code that prohibits creditors from taking or continuing to prosecute any collection action against you such as harassing telephone calls, repossessions, garnishment of wages/bank accounts, and foreclosures. If a creditor violates the automatic stay, it can be sued and sanctioned for monetary damages.

About 30 to 45 days after a case is filed, you will have a bankruptcy hearing with the trustee and one of our attorneys will appear with you. The hearing usually lasts only 5 to 10 minutes, but you will be sworn under oath to testify truthfully about your assets and debts. The trustee will ask you to answer a series of questions in order to determine if the information and representations in your bankruptcy petition schedules are accurate.

About 60 days after your bankruptcy hearing and provided all information and representations in your bankruptcy petition and schedules was accurate, the bankruptcy court will issue a discharge order in your favor. The discharge order is an order of the bankruptcy court that is permanently binding upon your creditors and which permanently nullifies or discharges your legal responsibilities to pay them.

There are a few types of debt that will usually not be discharged by a chapter 7 discharge. For instance, certain tax debts, child support debts, student loan debts, debts owed to employees, and debts incurred through fraud or embezzlement, and debts incurred through the use of a motor vehicle while intoxicated will generally not be discharged.

The issuance of a discharge order by the bankruptcy court is the start of a new credit beginning—a fresh start, if you will—for you. This debt relief is the “product” that you purchase by filing a bankruptcy. Typically, you will receive many credit solicitations after your case is concluded. At Behm Law Group, we call this the “Pinocchio Effect” because you will have little or no “debt strings” after your case has concluded. New creditors will send you solicitations because they will no longer have to compete with your previous creditors who were discharged in your bankruptcy.

Bankruptcy law requires that you complete two financial courses, one before your case can be filed and one after your case has been filed. Both of these courses can be done either over the telephone or over the internet and you will be issued certificates of completion for each course which must be filed with the bankruptcy court. The first course you will take is a pre-bankruptcy course called credit counseling which is designed to help you review and evaluate your financial situation. The second course, called debtor education, is taken after your case is filed and you must complete it in order to receive your chapter 7 discharge. This course is designed to help you better prepare for your financial future, and you will receive tips on things such as how to budget better and how to distinguish “good debts” from “bad debts.”

After your liquidation bankruptcy has concluded, it will be prudent for you to actively do things to further repair your credit such as getting a vehicle loan or getting one credit card and making sure you pay it off every month or just paying your monthly bills, such as utility charges and rent or house payments on time. About six to nine months after your bankruptcy has concluded, you should pull your credit report from a credit reporting agency such as Equifax, Experian or Trans Union to be sure that the creditors listed in your bankruptcy are reporting their claims properly in your credit file. Any such claim that was included in your bankruptcy should be reported as “Account Included in Bankruptcy” or some other such language. If any claims are not so listed, you will need to contact one of our

attorneys to possibly sue any creditors who may be improperly and unlawfully misrepresenting the status of their claims in your credit file.